Cat Bonds: When Markets Finance the Unpredictable

From interest rates to tornado risk

"Historically, cat bonds have exhibited lower volatility than many other financial assets, all while delivering returns that are comparable to those of equities."

In an environment where diversification is increasingly difficult to achieve and correlations between traditional assets tend to converge during periods of stress, investors are turning to more atypical segments. Among these, catastrophe bonds, or “cat bonds,” occupy a unique space: their performance depends less on economic cycles than on the hazards of nature.

In theory, these bonds can apply to a wide range of risks, from terrorism to cyberattacks, as well as longevity risk and pandemics. However, in practice, approximately 95% of this growing market of more than 60 billion dollars remains concentrated on natural disasters.

Turning a Hurricane into a Financial Product

The principle behind cat bonds is based on a relatively simple idea: transferring insurance risk to financial markets.

Risk Transfer: When an insurer or reinsurer wants to protect themselves against a major event—such as a hurricane in Florida or an earthquake in Japan—they can choose to cede a portion of that risk to investors through a dedicated structure.

Capital & Collateral: This structure issues a bond where the capital provided by investors is invested in liquid, low-risk assets, generally short-term instruments known as collateral.

The Coupon: In return, investors receive a coupon consisting of a risk premium paid by the insurer, plus the yield generated by the collateral.

While this sounds very similar to a classic bond product, the essential difference lies in the condition attached to the yield. If the contractually defined event occurs during the life of the product, a portion—or even the entirety—of the capital can be mobilized to cover the insurer’s losses.

A Source of Return... Independent of the Markets

It is precisely this dependence on an exogenous event that constitutes the primary appeal of cat bonds. Unlike corporate bonds, their performance is not linked to an issuer’s solvency, interest rate fluctuations, or equity market movements. Instead, it depends primarily on whether or not a physical risk actually occurs. In a diversified portfolio, this characteristic offers a tangible advantage. During periods of financial tension, traditional assets often move in lockstep, which undermines the effectiveness of diversification. Cat bonds, however, follow a different set of rules: a market crash, in principle, has no direct bearing on the likelihood of a hurricane. This relative independence is why they are frequently included in “liquid alternative” strategies or multi-asset portfolios looking for true diversification.

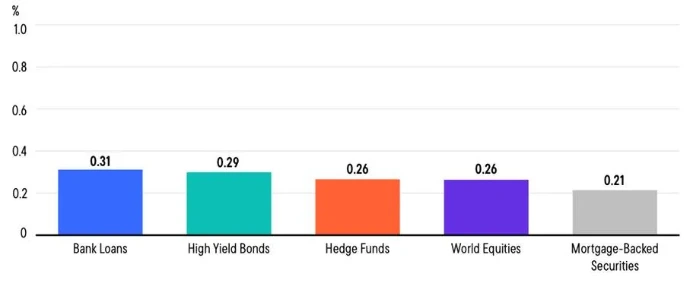

Cat Bonds Have a Low Correlation to Traditional Asset Classes (July 2004–July 2024)

Source: Franklin Templetion as of September 2024, Bloomberg, various index providers as listed.

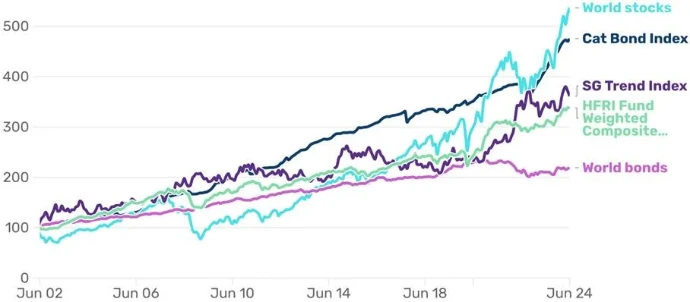

From a performance standpoint, investors have been rewarded for the uncertainty and the more restricted liquidity associated with these instruments. Historically, cat bonds have exhibited lower volatility than many other financial assets, all while delivering returns that are comparable to those of equities.

Performance of cat bond indices versus stocks and bonds

Source: Man Group database, MSCI and Bloomberg.

Diversification Under Constraint: An Asymmetry to Master

On paper, cat bonds present undeniable advantages within an asset allocation. Their low correlation with traditional assets makes them an attractive source of diversification, capable of improving a portfolio’s risk-return profile. However, this promise is built on a more nuanced reality. Unlike a traditional bond, where risk typically materializes progressively—through a credit downgrade, for example—cat bonds introduce a form of sudden rupture. For long periods, they can generate regular and relatively stable income. Yet, in the event of a trigger, the loss can be immediate and significant. This asymmetric profile, characterized by frequent gains and rare but potentially high losses, aligns these instruments more closely with insurance logic than with traditional bond investing. The investor is not compensated for a classic financial risk, but for accepting an extreme hazard that is, by nature, difficult to anticipate.

Evaluating this risk is, in fact, one of the primary challenges. It relies on sophisticated models combining historical data and simulations, whose reliability—while constantly improving—remains imperfect. This is especially true as the frequency and intensity of natural disasters can evolve non-linearly, particularly in the context of climate change. In this environment, risk management cannot be limited to simple exposure to the asset class. It requires fine diversification across issuers, structures, types of perils, and geographic zones to avoid excessive concentration on a single event or region. Integrated thoughtfully within such an approach, cat bonds can provide real added value. Conversely, a poorly calibrated or insufficiently diversified exposure can lead to unexpected losses.